|

|

|

|

|

|

#1

01-30-2015, 04:17 PM

01-30-2015, 04:17 PM

|

||||

|

||||

|

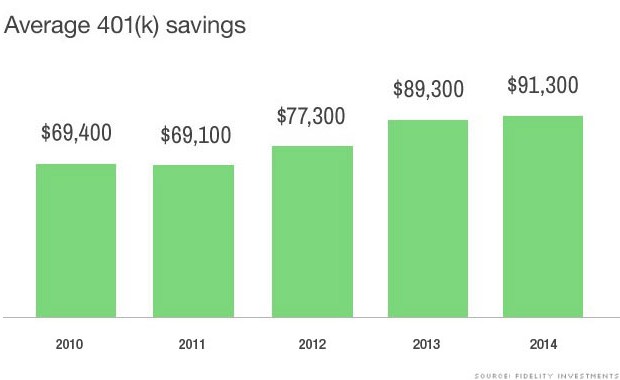

Average 401(k) Account is $91,300.00

|

|

#2

01-30-2015, 04:37 PM

|

||||

|

||||

|

Counterpoint.

31% of Americans have no retirement savings at all. 31% of Americans have no retirement savings at all - Aug. 8, 2014 and though my 401K is well above "average", I nevertheless have growth vs safety concerns.....and RMDs are just over the horizon.

|

|

#4

01-30-2015, 04:53 PM

|

||||

|

||||

|

Quote:

|

|

#6

01-30-2015, 05:56 PM

|

||||

|

||||

|

91K doesn't seem like it would last very long, at least not in this country.

__________________

You're a daisy if you do. __________________________________ 84 Euro 240D 4spd. 220.5k sold  04 Honda Element AWD 1985 F150 XLT 4x4, 351W with 270k miles, hay hauler 1997 Suzuki Sidekick 4x4 1993 Toyota 4wd Pickup 226K and counting

|

|

#7

01-30-2015, 06:21 PM

|

||||

|

||||

|

Don't forget there are a ton of people with young 401k accounts.

__________________

TC Current stable: - 2004 Mazda RALLYWANKEL - 2007 Saturn sky redline - 2004 Explorer...under surgery. Past: 135i, GTI, 300E, 300SD, 300SD, Stealth

|

|

#9

01-30-2015, 07:21 PM

|

||||

|

||||

|

Quote:

|

|

#10

01-30-2015, 08:32 PM

|

|||

|

|||

|

Quote:

__________________

1977 300d 70k--sold 08 1985 300TD 185k+ 1984 307d 126k--sold 8/03 1985 409d 65k--sold 06 1984 300SD 315k--daughter's car 1979 300SD 122k--sold 2/11 1999 Fuso FG Expedition Camper 1993 GMC Sierra 6.5 TD 4x4 1982 Bluebird Wanderlodge CAT 3208--Sold 2/13

|

|

#11

01-30-2015, 10:29 PM

|

||||

|

||||

|

The bad news: most people will need far more than that for a comfortable retirement. The common 4% rule for example, dictates that $250,000 would provide only $10,000 a year in retirement income.

Of course, 401(k) balances are just a snapshot of the retirement savings landscape since savers often have multiple investments and accounts like Individual Retirement Accounts (IRAs) and annuities. Fidelity, for example, found IRA holders had an average balance of $92,200 in 2014

|

|

#12

01-30-2015, 11:03 PM

|

|||

|

|||

|

I found this in a report on California's retirement system:

Even if employees in a DC plan do manage to earn the same rate of return as a DB plan fund and resist the urge to cash out prematurely, at the end of a full career they will likely receive a smaller benefit than similar employees in the DB plan. For example, an employee in a DB plan (with a benefit formula of 2% at age 60 and employer and employee contributions of 10% of pay) hired at age 30 with a starting salary of $25,000 and 5% pay increases each year will have a retirement benefit with a present value of $732,100 upon retirement at age 60. In contrast, the retirement benefit for an employee in a DC plan hired at the same age with the same salary (assuming that the DB plan and DC plan both earn a rate of return of 8%) will have a present value of $497,529 upon retirement at age 60.

__________________

1977 300d 70k--sold 08 1985 300TD 185k+ 1984 307d 126k--sold 8/03 1985 409d 65k--sold 06 1984 300SD 315k--daughter's car 1979 300SD 122k--sold 2/11 1999 Fuso FG Expedition Camper 1993 GMC Sierra 6.5 TD 4x4 1982 Bluebird Wanderlodge CAT 3208--Sold 2/13

|

|

#13

01-30-2015, 11:08 PM

|

|||

|

|||

|

The whole analysis is here: http://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=8&ved=0CEwQFjAH&url=http%3A%2F%2Fwww.calpers.ca.gov%2Feip-docs%2Fmember%2Fretirement%2Finfo-sources%2Fdefined-bene-facts.pdf&ei=OVLMVLSVNcScgwT8poHIBg&usg=AFQjCNHstdakG8V75rdsjhP73U6c6tWJvA

__________________

1977 300d 70k--sold 08 1985 300TD 185k+ 1984 307d 126k--sold 8/03 1985 409d 65k--sold 06 1984 300SD 315k--daughter's car 1979 300SD 122k--sold 2/11 1999 Fuso FG Expedition Camper 1993 GMC Sierra 6.5 TD 4x4 1982 Bluebird Wanderlodge CAT 3208--Sold 2/13

|

|

#14

02-01-2015, 04:00 PM

|

|||

|

|||

|

There are many ways to consider what you feel will be required in retirement. Plus many ways to do it.

The ways will change with the generations. It becomes an equation with a lot of variables or intangiables . Mind the aspect that nobody really knows the future. Doing something is still mandatory of course. I expect interest will remain very low for the next decade or two yet there is no way to be sure. Other than it might impact earnings on investments. Inflation has been pretty constant over our working years. The severity or lack of severity in the future is yet another serious potential issue. Assuming the buying power in the future is the really dangerous component. For example what we as a couple could actually live on twenty years ago probably would only cover the groceries today is pretty much factual in Canada anyways. Last edited by barry12345; 02-01-2015 at 04:25 PM.

|

|

#15

02-01-2015, 11:06 PM

|

||||

|

||||

|

Quote:

I also know (numerous) people that became multi-millionaires during the recession.  . Last edited by Skid Row Joe; 02-02-2015 at 12:15 AM.

|

|

| Bookmarks |

| Thread Tools | |

| Display Modes | |

|

|

Linear Mode

Linear Mode